How to Manage Your Student Loans

Common Questions

If Navient reported inaccurately, yes. When information is reported accurately, the Fair Credit Reporting Act does not permit Navient to provide courtesy retractions of information reported to consumer reporting agencies.

Interest accrues daily on student loans and Unpaid Interest may be capitalized (added to the principal balance) as permitted by law and your loan agreement.

Capitalized interest increases both the principal balance and total loan cost.

Typically, interest may be capitalized at the end of a grace/deferment/forbearance period or when the loan enters repayment (as often as quarterly during in-school, grace, or deferment periods).

Tip! You can help avoid capitalized interest by making interest payments even when you don’t have payments required (e.g., in school) or avoiding deferment and forbearance options altogether.

To view a full transaction history, log in to your Navient online account and go to your "Account History". From there you can review how past payments were applied (typically applied to Unpaid Fees, then Unpaid Interest, and lastly Unpaid Principal), fees assessed, and changes to your balance (including capitalized interest).

If you’re a federal loan borrower, you may be eligible for Public Service Loan Forgiveness (PSLF). Contact our public service specialists or go to StudentAid.gov to learn about PSLF and other programs – such as Temporary Expanded Public Service Loan Forgiveness (TEPSLF), which for a limited time may give you credit for past periods of repayment (while you were working for a qualified employer) that previously did not count toward PSLF.

Interest rates on federal student loans are set by Congress, whereas interest rates on private loans are set by the lender at the time of loan origination.

The interest rate may be variable or fixed for the life of the loan, depending on the terms of your promissory note.

Learn about student loan interest.

Important: Variable interest rates for federal loan borrowers can change annually (typically July 1st) and impact the amount you pay. Your student loan servicer does not set your interest rate and cannot change it. While calculations on variable rate student loans vary dependent upon your loan type, their rates are based on the 13-week T-Bill auction. Learn more about these FFELP rate changes.

You can always pay more than your Monthly Payment Amount, online or by U.S. Mail. By paying more now, you could pay less over the life of the loan.

If you’re enrolled in Auto Pay, you can add an additional amount to be transferred each month. Log in, select Auto Pay in the left menu, and follow the instructions.

Once all required documentation is received, it will take up to 15 business days to process your new repayment plan.

You’ll receive an email from us (or letter, if you’re not signed up for eDelivery) when we have an update for you about the status of your request.

The terms and conditions of private student loans provide for the potential release of a cosigner, which is contingent on the satisfaction of certain criteria and submission of a completed Application to Request Release of Cosigner(s) from Private Education Loans.

For 20 and up to 60 days after a loan is paid in full, the status may continue to reflect In Repayment online.

There could be many reasons for this, but it’s likely due to capitalized interest.

Interest accrues daily on student loans and Unpaid Interest may be capitalized (added to the principal balance) as permitted by law and your loan agreement.

Capitalized interest increases both the principal balance and total loan cost.

Typically, interest may be capitalized at the end of a grace/deferment/forbearance period or when the loan enters repayment (as often as quarterly during in-school, grace, or deferment periods).

Tip! You can help avoid capitalized interest by making interest payments even when you don’t have payments required (e.g., in school) or avoiding deferment and forbearance options altogether.

To view a full transaction history, log in to your Navient online account and go to your "Account History". From there you can review how past payments were applied (typically applied to Unpaid Fees, then Unpaid Interest, and lastly Unpaid Principal), fees assessed, and changes to your balance (including capitalized interest).

It depends as there is very strict eligibility criteria.

This settlement agreement was reached and includes cancellation for certain defaulted private student loans that attended for-profit schools that are now closed given the federal government stopped lending to them.

To be eligible, all of the following must be applicable to you:

- Borrowed a private loan between 2002 and 2010

- Defaulted on your private loan prior to 6/30/2021

- Attended a for-profit school that is now closed

Important! Federal loans are not eligible for this forgiveness. However, some states are providing payments directly to certain borrowers through a separate Consumer Fund. The states, not Navient, choose who will receive these funds.

Learn more about this settlement at Navientagsettlement.com.

The U.S. Department of Education (ED) has announced that it will make adjustments to Income-Driven Repayment (IDR) plan payment counters. For a limited time, FFELP loan borrowers can only benefit from the adjustment by consolidating into a Direct Consolidation loan on or before April 30, 2024. You can learn more at StudentAid.gov.

If a payment due date falls on a weekend or holiday, it's possible to experience a delay on the payment extraction from your financial institution.

Payments will be posted effective as of the due date and no late fees will be assessed. Please allow 3 days for your payment to post.

If you have eligible deferment time, a deferment is recommended over forbearance.

For eligible federal subsidized loans, you may not be responsible for interest that accrues during deferment.

You're responsible for the interest that accrues during deferment on all other loans (unsubsidized federal and private) and during forbearance.

Learn about repayment options for federal loans and private loans.

Go to About Payments to learn how to pay with special instructions, how payments are allocated and applied, and view a payment glossary.

Making Payments

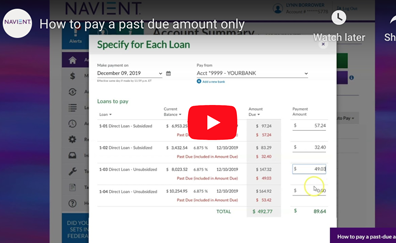

Pay Only Past Due Amounts

Log in and select Custom Pay > Specify for Each Loan.

Input the past due amounts, which are displayed in red in the Amount Due column.

Select Preview to check your inputs.

Select Submit to make the payment.

Download a PDF that shows you how

See how it’s done:

Change Your Payment Due Date

First, you must be in repayment and your account must be current.

Log in and select Help Center in the left menu.

At the bottom of the page, select Email Navient with your question.

Select Loan Type, then Change my due date.

Input the requested due date.

For federal student loans, request a date between the 1st and 28th of the month.

For private student loans, request a date between the 3rd and 22nd of the month.

Select Submit to send your request. We’ll confirm the change within 2-4 business days.

If your current due date is too close to the one you requested, we may have to make the change effective for the next month’s payment, and you may need to make one more payment by the current due date.

Get the Status of a Payment

Log in and view the status of payments you made in the Recent Payments list on the Account Summary.

You can also view details about payments in Account History.

Your payment will be credited as of the scheduled electronic payment date or the date the mailed payment was received.

Online payments made by 11:59 PM ET will be credited effective as of the current date – including weekends and banking holidays.

If you're enrolled in Auto Pay, your payment will be effective on your due date.

Please allow time for if you are sending the payment by U.S. Mail, and keep in mind that mailed payments are only processed on business days.

Please allow at least 2 business days for processing, from the scheduled date for electronic payments or the date delivered for mailed payments.

If you made a payment on a weekend or holiday, you might not see your payment reflected online yet – and the loan status in the Your Loans list may display the loan as Past Due. If that’s the case, please allow an additional day for your payment to clear. Once it is processed, your payment will be credited effective as of the scheduled payment date.

When Payments Increase

Monthly payment amounts can increase when:

Unpaid interest is capitalized – added to your unpaid principal balance – causing the interest to accrue on a higher balance, making your payments higher.

Your loan has a variable interest rate and the rate increases.

You've changed repayment plans.

You elected a plan that temporarily lowered your payments for a period of time, which has now ended.

Your loan will not be paid in the remaining term due to past periods of delinquency or inconsistencies in your payment history.

Auto Pay

Enroll in Auto Pay

Log in and select Auto Pay in the left menu.

Select a bank account or add a new one.

Deselect any loans you don’t want to enroll.

Input the amount you’d like to pay toward each loan.

Select Preview to check your inputs.

Select Submit to enroll.

Loans need to be current and in active repayment to be enrolled in Auto Pay. This includes loans in deferment or forbearance.

Federal student loan borrowers can download the form.

Private student loan borrowers, call us to enroll in Auto Pay.

Add or Remove a Bank

Log in and select the Profile icon and Edit Your Profile – or select the person icon or your name at the top of the page.

On the Profile page, scroll down to the Bank section.

Select Remove this bank or Add a new bank and follow the instructions.

If you remove a bank that’s enrolled in Auto Pay, your Auto Pay will also be canceled, and you will lose benefits associated with it.

To change a bank that’s in Auto Pay, you need to cancel your current Auto Pay and reenroll.

Change or Cancel Auto Pay

To change a bank that’s in Auto Pay, you need to cancel your current Auto Pay and reenroll.

Log in and select the Profile icon and Edit Your Profile – or select the person icon or your name at the top of the page.

On the Profile page, scroll down to the Bank section.

Select Cancel Auto Pay below the details of the current Auto Pay and select Yes.

To reenroll, select Auto Pay in the left menu and follow the instructions.

Depending on when you cancel and reenroll, you may need to make a manual payment to keep your account current.

You can cancel Auto Pay up to 3 business days before a scheduled transfer.

Add More to Your Auto Pay Amounts

Log in and select Auto Pay in the left menu.

Input the amount you’d like to pay toward each loan.

Select Preview to check your inputs.

Select Submit to change your amounts.

You can change the amount at any time prior to when the transfer is initiated, about 5 days before the due date.

Payment Instructions

Pay with a Debit Card

Call 888-272-5543.

Say "Make a payment" and follow the system prompts.

Make a Payment from Outside the U.S.

We ONLY accept payments in U.S. funds.

Here are some options available for making a payment from outside the U.S.:

International money order in U.S. currency drawn on a U.S. bank in U.S Dollars, which must be pre-printed on the money order or check

International money transfer that pays out in U.S. currency

Payment made from a U.S. currency account

Payment made from a Canadian bank as long as the payment is in U.S. funds and the bank has a valid 9-digit ABA routing number

SWIFT or wire transfer (fees associated)

The Automated Clearing House (ACH) is the electronic payment system most commonly used for bank-to-bank transfers of consumer payments in the U.S. A bank account with an American Bankers Association (ABA) routing number is required for payment via ACH.

Find Out Where to Mail Your Payment

Go to Contact Us and select the type of loans you have.

If you don’t know the type of loans you have, log in and view them on your Account Summary or Loan Details pages.

Find the corresponding mailing address.

Be sure to include your remittance slip and write your full account number on your check – and include any special instructions on a separate piece of paper.

How Late Fees are Applied

A late fee may be charged according to a loan’s promissory note. You can avoid late fees by making payments on time.

When payments are received, they're typically applied first to any unpaid fees, then to unpaid interest, and then to unpaid principal.

If you have a federal loan in an Income-Based Repayment (IBR) plan, the payment goes first to unpaid interest, then to unpaid fees, and then to unpaid principal.

Go to About Payments to learn about late fees and how payments are allocated and applied.

Get a Loan Payoff Amount

Log in and select a loan or select Loan Details in the left menu and then select a loan.

Ready to pay off this loan today? provides your payoff amount.

The U.S. Mail payoff amount includes an additional 10 days of estimated interest accrual, because interest accrues daily and you are responsible for interest accrued until the final payment is received.

If you mail your payment and it takes less than 10 days to reach us, you'll be refunded anything above the final payoff amount. If it takes 10 days or more to reach us, you may owe more due to interest accrual, interest capitalization, variable interest rate changes, and/or late fees.

Payment Allocation

Payment Allocation and Application

Allocation is how a payment is distributed across multiple loans.

Application is how the amount is applied based on the terms of the loan’s promissory note. Your payment may be allocated and applied differently depending on whether you have a federal or private loan, the status of your loan, and if you have multiple loans that are combined into one billing or loan group.

Go to About Payments to learn how payments are allocated and applied.

Auto Allocate an Overpayment Across Loans

Log in and select Custom Pay > Auto Allocate.

Input the overpayment amount, deselect any loans not to pay, and select Next.

Specify the allocation method for this overpayment.

Select Preview to check your inputs.

Select Submit to make the payment.

Go to About Payments to learn how payments are allocated and applied.

Auto Allocate an Underpayment Across Loans

Log in and select Custom Pay > Auto Allocate.

Input the underpayment amount, deselect any loans not to pay, and select Next.

Specify the allocation method for this underpayment.

Select Preview to check your inputs.

Select Submit to make the payment.

Go to About Payments to learn how payments are allocated and applied.

Specify a Default Payment Direction

Log in and select the Profile icon and Edit Your Profile – or select the person icon or your name at the top of the page.

On the Profile page, select the blue edit icon next to Payment Directions or select Change your payment directions.

Choose your preferred overpayment allocation, underpayment allocation, and billing direction.

Select Submit to save your changes.

Go to About Payments to learn how payments are allocated and applied.

Apply For

An Income-Based Repayment (IBR) Plan

For federal loans only:

If you’ve forgotten your FSA ID or password, follow the instructions to reset them.

Be sure to have your IRS information ready so proof of income can be pulled in automatically.

If you can’t import your IRS data, provide proof of income as instructed.

If you need to provide proof of income separately, log in to securely upload or mail it to:

Navient

Attn: Credit Bureau Management

P.O. Box 9655

Wilkes-Barre, PA 18773-9655

You’re required to recertify and provide proof of income annually. Watch for communications from us to remind you.

Need help? Check out this useful guide on how to complete the IDR online application.

A Different Repayment Plan

For federal loans:

Log in and select Repayment Options in the left menu.

Go to “Help me select a repayment plan that’s right for me.”

Select the Explore Federal Loan Repayment Plans button.

Input and submit your family size and income information.

View each plan you’re eligible for by choosing from the dropdown or using the Next and Previous links at the bottom of the page.

Follow the instructions – go to StudentAid.gov to apply for an Income-Driven Repayment (IDR) plan or download the IDR plan request form.

For private loans, contact us at 888-272-5543 to see what options your loan is eligible for.

Learn about repayment options for federal loans and private loans.

A Deferment

For federal loans:

Log in and select Repayment Options in the left menu.

Go to "I need to stop making payments for a while."

Select your circumstances, and then choose your specific situation.

Answer the online questionnaire and submit your deferment request.

Follow the instructions for submitting additional documentation, if required.

For private loans, contact us at 888-272-5543 to see what options your loan is eligible for.

Learn about deferment options for federal loans and private loans.

An In-School Deferment

For federal loans:

Log in and select Repayment Options in the left menu.

Go to "I need to stop making payments for a while."

Then go to "I’m in school – or a fellowship program, internship/residency, parent of student, or school teacher."

Choose your specific situation.

If you select "I am enrolled at least half time at an eligible school," you may not need to submit your request, especially if your school participates in the National Student Clearinghouse or NSLDS database – because Navient checks them both for students who have returned to school.

You can also download the form, get it certified by an authorized official at your school, then log in and select Inbox / Upload in the left menu to upload your completed form.

For private loans, contact us at 888-272-5543 to see what options your loan is eligible for.

Learn about deferment options for federal loans and private loans.

Forbearance

For federal loans:

Log in and select Repayment Options in the left menu.

Go to "I need to stop making payments for a while."

Then go to "I don’t qualify for a deferment and need temporary relief – I’m interested in a forbearance."

Choose your specific situation.

Answer the online questionnaire and submit your forbearance request.

Follow the instructions for submitting additional documentation, if required.

Be sure you understand the impact of forbearance as you determine if this option is right for you. Learn more at StudentAid.gov.

For private loans, contact us at 888-272-5543 to see what options your loan is eligible for.

Learn about forbearance options for federal loans and private loans.

Direct Loan Consolidation

For federal loans only:

If you’ve forgotten your FSA ID or password, follow the instructions to reset them.

Be sure to have your education loan records, account statements, and bills ready so you have all the information needed.

Navigate to the Direct Consolidation Loan Application and follow the instructions.

Military Benefits

For SCRA (Servicemembers Civil Relief Act) benefits:

Log in and select Tools & Requests in the left menu.

Select Servicemember Request Form.

Choose your situation and select Next.

Go to Inbox / Upload in the left menu to submit your supporting documentation.

For other benefits, contact our Military Benefits Team at 855-284-4879.

Learn about all available military benefits.

Loan Forgiveness and Discharge

Public Service Loan Forgiveness

Learn more about Public Service Loan Forgiveness (PSLF).

For federal loans only:

Use the PSLF Help tool to find out if you qualify.

Print the form, sign it, and provide it to your employer for certification.

Submit the completed form to the address on the form.

Teacher Loan Forgiveness

For federal loans only:

Download the form and input your information.

Print the form, sign it, and provide it to your CAO (Chief Administrative Officer) for certification.

Ensure all the CAO information is signed and complete.

Log in and select Inbox / Upload in the left menu to submit your completed form.

Need help? Check out these useful tips on how to complete the teacher loan forgiveness application.

Loan Forgiveness, Cancellation, or Discharge

For federal loans:

Go to StudentAid.gov to see if you qualify.

Find the form you need, download it, and input your information.

Print the form and sign it.

Log in and select Inbox / Upload in the left menu to submit your completed form to Navient.

Completed forms for federal loan Public Service Loan Forgiveness and Total and Permanent Disability discharge must be returned to the U.S. Department of Education’s servicer for these programs. Learn more at StudentAid.gov.

For private loans, contact us at 888-272-5543 to see what options your loan is eligible for.

Learn about loan forgiveness and discharge options for federal loans and private loans.

Discharge in Bankruptcy

If you file for bankruptcy, your loan may be discharged under certain circumstances.

Contact your legal counsel and/or financial advisor to see what your rights are under bankruptcy law.

Find Documents and Provide Documentation

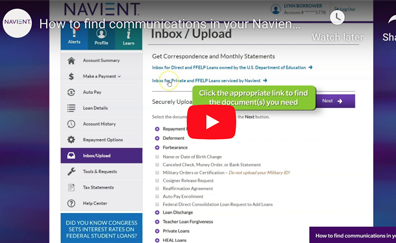

Get Monthly Statements and Correspondence

Log in and select Inbox / Upload in the left menu.

Select the Inbox link at the top of the page.

Select the PDF or IMG button to view your documents.

To see some documents you provided to us, select the Documents You Sent to Us tab — this page only displays certain documents we received within the last 7 calendar days.

Download a PDF that shows you how

See how it’s done:

Upload Forms and Documentation

Log in and select Inbox / Upload in the left menu.

Select the type of documents to upload, expanding the options as needed.

If the document is password protected, please remove that prior to uploading.

Browse your computer to find each document and select Upload File.

Be sure to select documents that are less than 5 MB in size.

When all documents are uploaded, select Submit Documents.

Download a PDF that shows you how

See how it’s done:

Send Forms and Documentation by U.S. Mail

Go to Contact Us.

Select the type of loans you have.

If you don’t know the type of loans you have, log in and view them on your Account Summary or Loan Details pages.

Find the corresponding mailing address.

Download Your Form 1098-E Tax Statement

Log in and select Tax Statements in the left menu.

Select the document to download by its tax year.

Submit a Reaffirmation Agreement

Download the form and input your information.

Print the form, sign it, and provide it to your school for completion.

Ensure all the school information is signed and complete.

Log in and select Inbox / Upload in the left menu to submit your completed form.

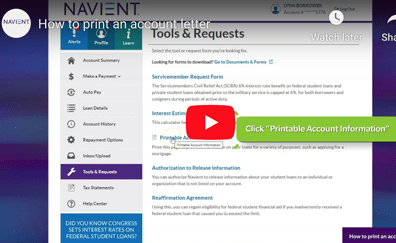

Print an Account Letter for a Mortgage Company or Other Lender

Log in and select Tools & Requests in the left menu.

Select Printable Account Information.

Print the document.

Download a PDF that shows you how

See how it’s done:

Manage and Update Your Account

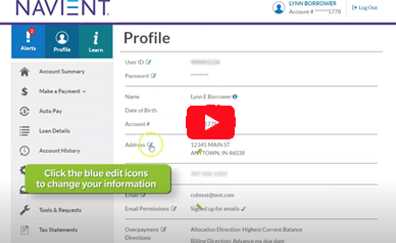

Update Your Profile Information

Log in and select the Profile icon and Edit Your Profile – or select the person icon or your name at the top of the page.

On the Profile page, select the blue edit icons to update specific information.

Select Submit to save your changes.

Download a PDF that shows you how

See how it’s done:

Estimate Your Interest Payments

Log in and select Tools & Requests in the left menu.

Select Interest Estimator.

Choose up to 31 days in the future and select Calculate.

Save Your Account History for Your Records

Log in and select Account History in the left menu.

Choose the view you want from the Display and Date Range dropdowns.

Choose Export or Print by selecting the icons above the table.

Find Out Which Borrower Benefits Your Loans Have

Depending on the type of loan, there may be borrower benefits available, such as repayment incentives that can lower your interest rate.

Log in and select the loan name on the Account Summary or select Loan Details in the left menu.

The information is in the Loan/Borrower Benefits section.

If your loan displays no borrower benefits, that means the loan isn’t eligible for benefits at this time.

Authorize Us to Provide Information to a 3rd Party

Log in and select Tools & Requests in the left menu.

Select Authorization to Release Information.

Input the 3rd party information and select Submit.

Submit a Name Change or Birthdate Correction

Log in and select the Profile icon and Edit Your Profile – or select the blue person icon or your name at the top of the page.

On the Profile page, select the blue info icon next to your name or date of birth to find out which documentation you need to submit.

Select Inbox / Upload in the left menu to submit your documents.

How to Read Your Statement

Visit our How to Read Your Statement page for a quick guide to help you understand your monthly statement.

If you're signed up for eDelivery, log in to access your statement online in your inbox.

Track Account Actions

Check the Status of a Request

You’ll receive an email from us (or letter, if you’re not signed up for eDelivery) when we have an update for you about the status of your request.

To view the update, follow the link in the email or log in and select Inbox / Upload in the left menu.

Select the Inbox link at the top of the page.

Select the PDF or IMG to view our communication to you.

Get Your Account Number

Log in and select the Profile icon or Account Profile below your name at the top of the page.

On the Profile page, next to Account #, select + show full number.

Select - hide to display only the last 4 digits again.

Your 10-digit account number is also viewable on the billing statements we’ve sent you.

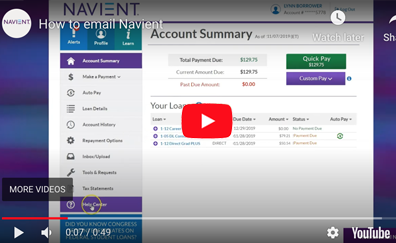

Email Us with Questions

Log in and select Help Center in the left menu.

At the bottom of the page, select Email Navient with your question.

If you have multiple loan types, indicate the one you’re emailing us about, or select All at the bottom.

Choose a category.

Type your question and select Submit.

One of our specialists will reply within 2 business days.

Log in and select Inbox / Upload to view their reply in your Inbox.

Download a PDF that shows you how

See how it’s done:

Find Out What Type of Loans You Have

Log in and view each loan’s Type in the Your Loans list.

Or select the Loan Name to view the Loan Details.

Scroll down to see the Loan Type – select the blue info icon there to learn more about the types of loans.

Find Out Which Repayment Plan Your Loans are in

Log in and select a loan or select Loan Details in the left menu and then select a loan.

The Repayment Plan is listed at the top of each Loan Details page.

View Your Declining Balance

Log in and select Account History in the left menu.

From the Display dropdown, select By Loan.

View the Unpaid Principal column for each loan’s declining balance by selecting the loan from the dropdown.

Student Loan Basics Videos

What can I do if I’m having trouble making my payments?

Long- and short-term plans as well as other programs are available if you are having financial issues.

What happens if I don’t make my payments?

Learn about delinquency and default and how to keep your loans in good standing.

Repayment timeline

What to expect while in school and in repayment.

Terms to know — the 3 parts of a loan

Learn about principal, interest, and fees and how they add up to your current balance.

How interest accrual works

Learn how interest will affect your loan repayment.